Nvidia Overtakes Apple as TSMC’s Biggest Customer — Why It Matters for Chips and Prices

This caught my attention because it’s a rare moment when a single customer shift at the world’s largest contract foundry signals a broad change in the semiconductor landscape – from smartphone dominance to an AI-first demand curve.

Nvidia beats Apple to become TSMC’s largest customer – and the chip world notices

- Nvidia is reported to have overtaken Apple as TSMC’s biggest customer, driven by soaring AI GPU demand.

- Jensen Huang confirmed Nvidia is now TSMC’s largest customer on a podcast, but did not provide exact figures.

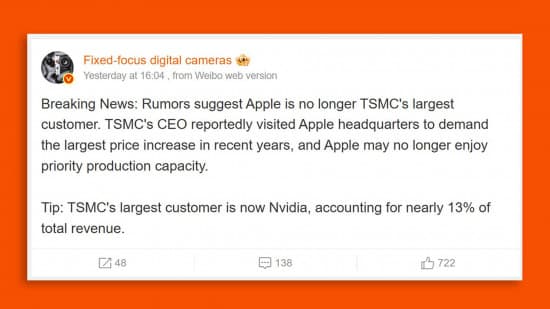

- A Weibo rumor pins Nvidia at ~13% of TSMC revenue (up from 11% in 2024) while Apple fell from ~24% – numbers are unconfirmed.

- The practical implications: tighter capacity for advanced nodes, higher ASPs for AI chips, and potential pricing/priority impacts for phone SoCs and gaming GPUs.

{{INFO_TABLE_START}}

Publisher|Discover

Release Date|2026-01-21

Category|Semiconductors / Industry

Platform|TSMC manufacturing (advanced nodes)

{{INFO_TABLE_END}}

What happened — the facts (and the fuzz)

Jensen Huang, Nvidia’s CEO, said on the “A Bit Personal” podcast that Nvidia is now TSMC’s largest customer — a strong confirmation of a shift that had been evident from market chatter. Huang stopped short of giving numbers. Separately, a Weibo account called “Fixed-focus digital cameras” circulated figures suggesting Nvidia’s share rose to ~13% of TSMC revenue from 11% in 2024, while Apple’s share dropped from roughly 24% in 2024. These social-media-sourced numbers should be treated as rumors until TSMC or the companies confirm them.

FinalBoss // Gear

Level up your setup

01Graphics cardson Amazon→02Gaming laptopson Amazon→03High-refresh gaming monitorson Amazon→04Discounted game keyson Kinguin→Affiliate links · As an Amazon Associate, FinalBoss earns from qualifying purchases.

Why this isn’t just a numbers story

Even if the precise percentages are uncertain, the underlying trend is unmistakable: cutting-edge demand has shifted. Nvidia’s business has ballooned because of datacenter AI accelerators that require the latest process nodes and long production runs. Those AI accelerators command very high average selling prices (ASPs), which gives Nvidia more billing power at a foundry like TSMC.

TSMC’s revenue mix matters because it drives capacity allocation and pricing incentives. If a larger share of TSMC’s revenue comes from high-margin AI chips, TSMC has commercial incentive to prioritize those customers on constrained advanced-node lines. That can make life harder for other customers that also need the same nodes — Apple for flagship SoCs, AMD and Nvidia for gaming GPUs, and anyone else building on N3/N4/N5 equivalents.

Two important caveats: first, the rumor that TSMC’s CEO demanded a big price increase from Apple is unverified and should be read skeptically. Second, Apple’s apparent percentage decline doesn’t necessarily mean it’s ordering fewer chips — it may simply be that overall pie growth (driven by AI) dilutes Apple’s share.

How this could change the market — realistic scenarios

- Pricing pressure for advanced-node wafers: TSMC may be able to push higher prices if a larger part of its revenue comes from customers willing to pay premium ASPs for AI silicon.

- Production prioritization: AI accelerators could get earlier access to scarce capacity, stretching lead times for gaming GPUs and flagship phone SoCs during tight cycles.

- Design and sourcing responses: Big buyers (Apple, AMD) may accelerate diversification plans — more long-term contracts, staggered node mixes, or investment in alternative fabs like Samsung — but switching is expensive and slow.

- Consumer impact is indirect but real: potential higher prices or longer waits for the newest iPhones and GPUs if capacity and pricing shift materially toward datacenter AI demand.

What this means for readers

If you’re a gamer waiting for a price drop on GPUs, don’t expect immediate relief. The expensive AI-focused wafers are eating up advanced-node capacity and commanding higher prices, which reduces the room for discounting. For iPhone buyers, any direct price increase would probably be gradual; Apple absorbs costs and adjusts features, but higher production costs ultimately constrain margins or feed into retail pricing over time.

For industry watchers and investors, the headline is a confirmation that the semiconductor market’s center of gravity is shifting toward datacenter AI. That has been the pattern for months — this is another data point showing it’s not a fad.

TL;DR — the quick take

Nvidia’s rise to TSMC’s largest customer (confirmed by Jensen Huang) is less a sudden upset and more a milestone in an ongoing industry transition: AI accelerators are soaking up cutting-edge capacity and commanding premium pricing. The immediate numbers from social posts are unverified, but the strategic implication is clear — expect tighter advanced-node availability, higher wafer economics, and slower relief for smartphone and gaming GPU pricing unless TSMC expands capacity or other suppliers step up.

As someone who watches semiconductor cycles closely, I’m excited that AI demand is driving investment and innovation — but realistic enough to worry about the short-term supply and pricing fallout for the devices we actually buy.